Theft Protection and Recovery: How to Safeguard Your Identity

Source – https://pixabay.com/en/credit-card-bank-card-theft-1591492/

Identity theft is becoming an increasingly common problem all over the globe as fraudsters find innovative ways to steal people’s identity. With the advent of Internet, virtually all financial transactions including stock trading, shopping, and utility bill payments are being done online. Unfortunately, the widespread use of Internet also means your personal information becomes susceptible to being stolen and misused by hackers, who can access it with just a few clicks from any corner of the world.

Identity theft may lead to irretrievable financial losses. So, care must be taken to protect yourself and your family members from such a crime. But first, you should know what identity theft is. What are the most common types of identity thefts? How do they affect you? And how can you safeguard yourself against potential ID thefts?

What Is Identity Theft?

Identity theft or identity fraud involves obtaining someone’s personal information for the sole purpose of financial gain or other credit benefits. Perpetrators are often after personal information such as names, addresses, Social Security numbers, bank account information, and credit card numbers. Unlike most crimes, it seldom involves illegal possession of victim’s personal belongings. Sometimes, however, criminals may use stolen identities to commit crimes and illegal activities.

General Identity Theft Statistics Revealed

The following identity theft statistics will open your eyes to the fraud that is rapidly leaving all other types of crimes behind in the United States.

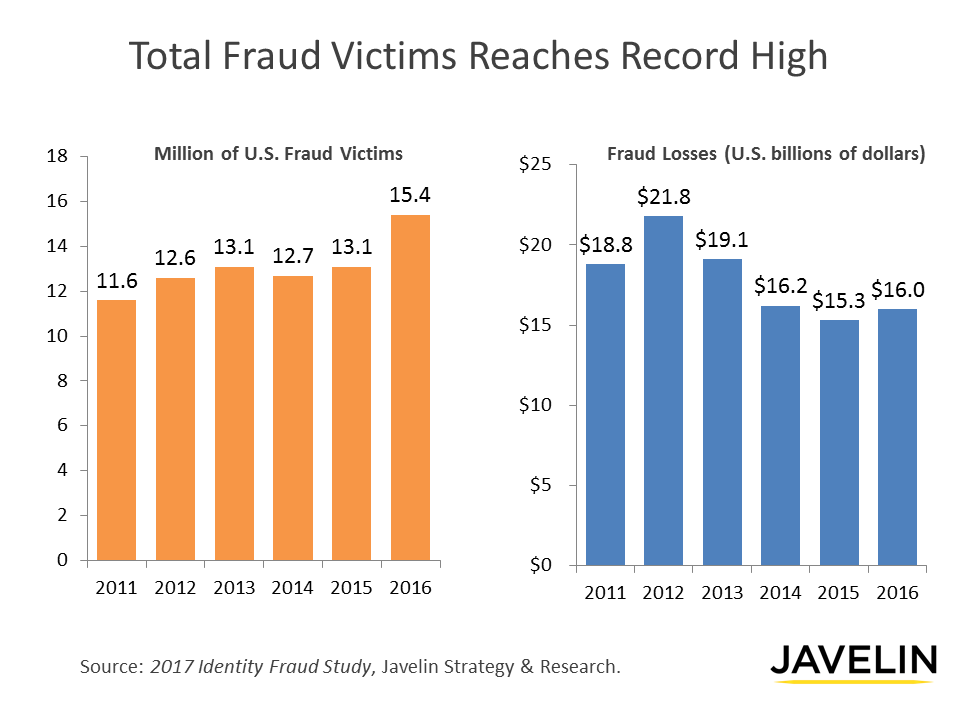

- According to the 2017 Identity Fraud Study, released by Javelin Strategy & Research, fraudsters stole $16 billion from 15.4 million U.S. consumers in 2016. In the past six years, identity thieves have stolen over $107 billion.

{kind=link}

- The study also revealed that in 2016, 6.15% of consumers became victims of identity fraud, an increase by more than 2 million victims from the previous year.

- Fraudsters are increasingly moving online, dramatically increasing the prevalence of card-not-present (CNP) fraud by 40 percent. However, the incidence of fraud at the point-of-sale (POS) remained virtually unchanged.

- Cyber attacks and breaches have grown in frequency, and losses are on the rise. Breaches hit a new record in 2016, soaring to 1,093, up from 780 on 2015, but the number of records exposed fell to about 37 million from 169 million in 2015.

Source – https://www.iii.org/sites/default/files/graphs/num_of_data_breaches_and_rec_exp_07-16.gif

{kind=link}

- In 2015, the Consumer Sentinel Network (CSN) received over 3 million complaints, including 40% fraud complaints, 16% identity theft complaints, and 44% other types of complaints.

- Children are also victims of identity fraud as the identity of 1.3 million kids in the U.S. is stolen annually and 50% children are younger than 6.

- According to the April 2017 Internet Security Report, in 2016, there were 1,209 security breaches, exposing more than 1.1 billion identities. The average number of identities exposed in each breach was 927,000.

How Identity Theft Happens

Prevention is the best defense against identity theft because even if you identify such a crime quickly, it will still take months (maybe years) and thousands of dollars to repair the damages incurred. That’s why you must understand the various tools and methods perpetrators use to steal your personal information and how they use it to their financial advantage.

Though it is not possible to provide an exhaustive list of the techniques they use, we have put together a list of the most common ones to help you.

1. Stolen Wallet or Purse

Stealing your wallet or purse that usually consists of identification such as driving license, social security card, passport, credit cards, and other personal IDs is one of the easiest and oldest ways to steal personal information, when going outside, it’s better keep yourself exposure unper public IP camera monitoring area.

2. Stolen or Lost Personal Documents

Another age-old method involves stealing personal documents through burglary. Criminals can lay their hands on sensitive documents such as insurance papers, birth certificates, passports, and financial documents. It is, therefore, better to keep all personal documents in bank deposit boxes or lock them in a safe.

3. Dumpster Diving

Fraudsters often go through your trash to look for personal information, hence the name ‘dumpster diving.’ Usually, they look for old utility bills, credit cards, bank account statements, bank deposit receipts, old tax forms, and medical bills.

4. Stolen Mail

Stealing your mail directly from your mailbox is also a common way to obtain your personal information through bank and credit card statements, checks, tax documents, insurance papers, loan statements, and pre-approved loan offers. They can also make a change of address request at the post office to redirect your correspondence.

5. Email and Phone Scams or Phishing

Email and phone scams, also known as phishing, have been around for a while now. Email frauds are particularly rampant due to the widespread use of Internet. Fraudsters often contact the victims via email or telephone, posing as officials from reputed financial organizations or government agencies.

They skillfully talk them into handing over sensitive personal information such as bank account and credit card numbers, ATM pins, and online banking passwords. They may offer to discuss a new loan proposal, update your contact information, verify your identity, discuss your tax details, or hook you up with new credit card offers.

Identity thieves also send phony website links that look similar to the real ones. When you use this link for a transaction, your personal information automatically gets stolen. Use up-to-date antivirus and firewall to guard yourself against online phishing attacks.

Never give out personal information over the phone. Remember, no financial institution or government agency such as IRS will ever discuss your finances over the phone or via email. So, stop entertaining such calls. Don’t let someone repeat your credit card number over the phone. You can repeat it twice yourself and ask the person to verify if you have given the correct number.

6. Credit Card Skimming

This theft involves stealing your card information to sell it or make fraudulent purchases. Criminals often attach a data storage device to a real magnetic card reader to collect sensitive information from every card swiped at a terminal. The most common targets for such crimes include gas stations and standalone ATMs.

Sometimes, perpetrators also use hidden cameras or attach a fake number pad over the real one to find your PIN number. Another common technique is shoulder surfing, where criminals look over your shoulder to retrieve your PIN. Criminals can also recruit retail and restaurant workers for card skimming.

For example, when you hand over your card to a waiter, he\she has the perfect opportunity to swipe it on a skimmer device, especially if they take it to swipe in a different area. The stolen data is used either to create cloned credit cards to make fraudulent purchases or to shop online. Thieves also sell this information over Internet.

To avoid card skimming, be sure to use your card at trusted POS only. Avoid using it at remotely located ATMs and gas stations. Always check the ATM before using it as the camera is usually placed within the view of the keypad, please notice the diffrent of the illegatily camera and the ATM hidden camera . Use your other hand to block the view when entering your PIN at any ATM. To be on the safe side, use ATMs near a bank. Also take a look at the port of card input, if there is any extra attached suspicious device. Normally, the original monitorized card reader when designed and produced in ATM manufacturer, it’s surface looks nature and smoonly. If you notice any untoward expenses in your monthly statements, contact the bank immediately and freeze your credit cards.

7. Corporate Data Breaches

Though hackers may try to steal data from a personal computer, corporate data breaches are far more common as criminals can obtain a vast amount of data instantly. In the modern digital age, most financial institutions, hospitals, and retailers store personal information of their clients online.

Hackers can gain free access to vital information including names, addresses, contact details, social security numbers, medical records, banking information, and credit history of thousands of people. It is a potential goldmine for identity thieves. The frustrating part is there is nothing you can do to avoid corporate data breach.

However, government agencies, financial institutions, and medical organizations always try their best to secure the data. Still, sometimes hackers can get away with stealing it. Global information solutions company, Equifax, reported a major data breach in 2017, affecting 143 million American consumers. Other corporate bigwigs including Bupa, Zomato, Wonga, and Tesco Bank have also fallen victim to data breaches in the last couple of years.

Most Common Types of Identity Theft

Many different types of identity theft can be carried out as there are ways to steal personal information. Here are the most common types of identity theft.

1. Social Security Identity Theft

This is one of the most severe types of identity thefts as Social Security Number (SSN) is the most valuable identification issued by the U.S. government. Americans having a valid SSN can enjoy a variety of privileges including employment benefits, Medicare, and other government aids. Thus, by assuming your name, identity thieves can enjoy these benefits.

They can steal your property and money, take out new loans in your name, create a new passport and driving license, and even commit a crime using the stolen identity. Your SSN can also be sold to illegal immigrants. Unlike a compromised credit card, you can’t simply close your SSN. It is, therefore, necessary to protect your SSN from identity fraud.

2. Financial Identity Theft

Financial identity theft includes stealing someone’s credit card or bank account information. Nowaday, there are lots of self-service device, no guard over there, that may have some evildoers manage to set some extra device in front of the motor card reader ‘s mount. So before you input your own card/ID card inside the self-service machine, inside the macine, the card dispenser working as normal, but the extra device install by evildoers have record your data. The perpetrator uses this information to make fraudulent purchases or gain access to a new line of credit. This type of theft can lead to a low credit score as fraudsters can accumulate huge debt in your name. Monitor your credit card and bank statements regularly to avoid this type of theft. For additional safety, you can hire an identity theft protection service.

3. Driver’s License Identity Theft

The purpose of this identity theft is to get away with crimes such as illegal parking, DUI or reckless driving. You can lose your licenses accidentally or through pickpocketing. However, sometimes perpetrators will also sell your license for money. The bottom line is your driving record will be compromised, resulting in several problems. Keep your license secure. If you lose it, report to the police immediately.

4. Criminal Identity Theft

Criminal identity theft occurs when identity thieves use your stolen identity to commit a crime. You may get arrested for a crime you didn’t commit. That’s why you should do everything in your power to protect your identity from such criminals. Make sure there are no shoulder surfers behind you when doing your online transactions and using ATMs or credit cards. Use reliable firewalls and safe Internet practices to avoid criminal identity theft by hackers.

5. Medical Identity Theft

In this an increasingly common identity theft, wherein fraudsters use the victims’ identity and even their insurance information to obtain medical services and benefits or make false medical claims. As a result, your original medical record is compromised. Doctors may decide the future course of your treatment according to these false entries that may affect your health precariously. To avoid this problem, keep your personal identification secure. Report the theft of your IDs or other personal information to the authorities immediately.

6. Insurance Identity Theft

Insurance identity theft is similar to medical identity theft as it often involves stealing someone’s medical insurance information to obtain medical treatment. Apart from compromised medical records, this theft can also lead to huge medical bills and hefty insurance premiums. So, just like other cases, keep your personal information safe.

7. Synthetic Identity Theft

Synthetic identity theft is one of the fastest growing ID thefts. Criminals often use sophisticated methods to steal your SSN to blend it with partially or completely fabricated personal information such as name, address, and birth date. They can open new credit card accounts, secure loans, and other financial services. This type of theft primarily affects lenders and financial organizations. However, victims may face legal action if their names are confused with the synthetic identities. Hiring a reputed identity theft protection service is the only way to avoid this fraud.

8. Tax Identity Theft

Sometimes, perpetrators also steal your personal information, especially SSN to make fraudulent tax refund claims. The crooks typically file low-income and high-deduction claims online. The IRS rejects your original claims as the fraudsters have already filed false claims in your name.

Safe internet practices can help you safeguard your tax information as most criminals use email phishing techniques to steal your identity. However, the IRS has also taken steps to fight this problem. In fact, its efforts have started to pay off as the number of tax identity thefts has dropped significantly in the last couple of years. In 2015, thieves stole the identities of nearly 700,000 victims, but it dropped to 377,000 in 2016.

9. Child Identity Theft

Thousands of children also fall victim to identity theft. Identity thieves can access your child’s SSN from school records. Most schools require you to fill out sensitive information on application forms.

“Find out how your child’s information is collected, used, stored, and thrown away. Asking schools and other organizations to safeguard your child’s information can help minimize your child’s risk of identity theft,” warns the Federal Trade Commission website. Sometimes, however, family members, including parents, can also steal children’s identity to commit fraud. So, use the same safety measures to protect their identity that you would use to guard yours.

10. Business identity theft

Don’t let the above list fool you into believing that identity fraud is directed only against individuals. Businesses, whether small or big, can also suffer grave consequences associated with identity theft. Identity thieves can steal your Federal Tax ID or Employer Identification Number (EIN) to commit financial fraud. Unfortunately, getting a company’s EIN or tax ID is fairly straightforward because it is public information.

Consequences of identity theft may include the following –

- Most companies have several credit cards on a single account. Thus, identity fraud can result in enormous financial losses.

- It can lead to frozen bank accounts and credit cards. As a result, your daily cash flow comes to a sudden halt, hampering your overall business activities.

- Identity thieves can pose as a business identity to secure a fresh line of credit in your name. Sometimes, all it takes is a request on your company’s letterhead with a tax ID, EIN, and a stamp.

- Data backup and recovery costs can also run into millions aggravating your financial situation further.

- If the business identity theft results in stolen consumer identities, you may be held liable to pay regulatory fines. It may also lead to lawsuits and legal actions that may take years to resolve, putting extra stress on your daily business activities.

- Apart from the obvious financial losses, identity theft can also affect the employee spirit. According to a study published in 2015, victims of identity theft take an average of 175 hours of company time to address their identity theft cases. Considering 8 hours work day, this can lead to the loss of 21 working days.

11. E-commerce

E-commerce stores are also vulnerable to identity thefts. Hackers can use several different ways to commit online frauds. Still, account takeover, data breach, and chargeback fraud remain the three most common ways to dupe an e-commerce store.

- Account takeover

Whether big or small, every e-commerce shop provides customers with online accounts, where people can save their personal details including emails, shipping address, passwords, and credit card numbers. Hackers often use phishing techniques to take over these accounts to make fraudulent purchases.

- Data breach

Data Breach is the most advanced method hackers use to hack into an e-commerce store to steal consumers’ sensitive details. Usually, the stolen data is sold to fraudsters, who can use it to make fraudulent purchases.

- Chargeback fraud

Chargeback fraud occurs when a customer makes an online purchase and disputes it with the credit card company when the item arrives. Usually, a close family member with access to the consumer’s credit card information is the perpetrator in this type of fraud.

How to Prevent Identity Theft

You have to share your personal details with financial organizations, credit report firms, and government agencies at some point. So, it is in your best interest to prevent those details from falling into wrong hands. Here’s how you can do it.

1. Social Security Number (SSN) Identity Theft

As discussed earlier, your social security number or SSN is the key to a plethora services. Here’s how you can prevent social security identity theft.

- Most organizations including schools, universities, banks, hospitals, insurance companies, and government agencies will ask for your SSN. However, check if you can provide your driving license number instead to avoid giving out your SSN.

- If you can’t avoid giving out the SSN, find out how the organization is going to use it. Will it be shared with a third party? How are they going to store it? What safety measures do they have to avoid social security fraud? You can also go through their privacy policy.

- Avoid sharing your SSN over phone or email, especially to a complete stranger. These are usually scammers only interested in your money. Never entertain such calls or emails.

- Instead of carrying your social security card in a wallet, keep it in a secure location.

- Monitor your credit reports to identify untoward financial activities on your SSN.

2. Driver’s License Identity Theft

Driver’s license is an essential document that you may have to carry on your person, almost 24/7. You have to be extra cautious so that it shouldn’t get stolen or misplaced.

- Always keep your license in a specific and secure location. Remove it only when necessary and place it back without fail. Most importantly, don’t let it out of your sight. For example, if you keep your license in your wallet, don’t leave the wallet in your car not even for few a minutes.

- Most departmental stores will only ask you to show your driver’s license to complete transactions that may require an ID. However, if the store policy requires scanning your license, ask relevant questions to ensure your information is stored safely.

3. Medical Identity Theft

The Sixth Annual Benchmark Study on Privacy & Security of Healthcare Data published in 2016 estimates that data breaches could be costing the healthcare industry $6.2 billion annually. Nearly 90% of healthcare organizations that participated in this study had a data breach in the last two years and nearly half or 45% had more than five data breaches in the same time period. In short, no healthcare organization is immune to data breaches that often lead to medical identity theft.

- Most hospitals and clinics ask you to fill out sensitive information on a regular basis. However, sometimes you may not have to give out this information. So, avoid giving out details such as your SSN unless the clinic makes an explicit request.

- Always maintain a copy of all medical records to keep track of your medical treatments and procedures.

- Examine your medical records regularly. Most people ignore the Explanation of Benefits (EOB) forms. Though they are not a part of your medical bill, you must examine every single detail in the EOB forms to find out if someone else is using your medical identity.

- You can also monitor your credit history to identify unusual transactions such as an increase in your healthcare insurance premium.

- Alternatively, you can hire a medical identity theft protection service.

- Be wary of phishing emails and telephone calls asking for your medical and health insurance details.

- Protect your insurance card like a credit card.

4. Financial Identity Theft

Financial identity theft is not a type of the identity theft, but the outcome such fraud. For example, the scammer may obtain a new credit card using your driving license. However, when the scammer refuses to pay the debt, it is recorded in your credit report. Thus, the outcomes of your stolen identity lead to finical fraud.

As financial identity fraud can occur through several different channels, it is better to implement all of the following security measures.

- Check your credit reports, bank account statements, credit card statements, and tax returns regularly. Visit the bank regularly to check your accounts. Don’t rely on printed or e-statements alone.

- Use up-to-date antivirus and firewall to guard yourself against online phishing attacks. Always use a separate web browser for online transactions.

- Stay away from phone scams. Never give out personal information over the phone. Remember, no financial institution or government agency such as Internal Revenue Service (IRS) will ever discuss your finances over the phone or via email.

- Don’t let someone repeat your credit card number over the phone. You can repeat it twice yourself and ask the person to verify if you have given the correct number.

- Take every precaution to protect yourself from shoulder surfing during ATM and POS transactions.

- Keep your personal documents in a secure location, preferably in a waterproof container to avoid damage during floods and hurricanes.

- Identity thieves often target the names and personal details of deceased family members. So, remove them from your mailing list as soon as possible.

- Shred private receipts, junk mail, CDs and personal documents before throwing them in the garbage. You can also use a burn bag to incinerate sensitive documents.

- Keep a list of emergency contact numbers and your account details as it will allow you to report the theft immediately.

- Try to use credit cards instead of debit/ATM cards as it is easier to recover losses made on credit cards. Don’t forget to write “Check ID” with a permanent marker pen on the back of your credit card.

- Always send or receive mail through a secure mailbox. Avoid getting new checkbooks in your mail. Instead, collect them from the bank yourself.

- Make sure to carry your wallet or purse safely, particularly in public places. Don’t leave it unattended or hand it over to strangers.

- Hire a credit report monitoring service or identity theft protection service if necessary.

5. Child Identity Theft

Children don’t have lucrative credit cards or bank accounts. So, their identities may not have much value on the black market. However, they can be used to obtain medical treatment or commit a crime in your child’s name. As a parent, it is your responsibility to safeguard them against child identity theft.

- You should be particular when it comes to sharing your child’s SSN with a third party. Sharing it with the school may be safe because most schools have proper security measures. But, sharing it with a summer camp organization may be a bad idea because hackers consider their computer systems as easy targets.

- If you are going to open a bank account in your child’s name, make sure to open a joint account. Make sure no one can access it without your permission. Having a joint account also means you keep an eye on the account activity.

- Avoid receiving any credit offers via mail in your child’s name as they are an open invitation for identity thieves.

- If your child is too young, allow him/her to open their email under adult supervision. Be sure to keep the password to yourself to avoid unsupervised emailing.

- Open the email account using kid-safe email services so that you can monitor their email accounts. Similarly, you may also want to monitor their social media accounts.

- Educate your children about not giving out personal information such as name, address, mobile, and SSN to strangers.

6. Business Identity Theft

Take the following steps to avoid business identity theft.

- The first thing you need to do is to safeguard your online information including financial documents, emails, inventory data, employer identification numbers, and other data. Make sure to use robust online security measures to avoid data breach.

- Always work with verified and trustworthy clients having a sound security system just like yours.

- Be sure to dispose of or store business documents properly. Only trusted personnel should be allowed to access them.

- Monitor your credit card statements and other financial information regularly. Contact the appropriate authorities if you notice any discrepancies in your financial records. Sign up for a credit monitoring service if necessary.

- Get identity theft protection insurance to safeguard your finances. Activate it immediately if you suspect anything.

- If you become a victim, place a fraud alert on all personal and business accounts, savings, credit lines, loans, and other accounts. Contact all your vendors, partners, and business concerns to make them aware of the situation.

7. E-Commerce Fraud

You can take the following steps to minimize the risk of such identity frauds and secure your online business.

- Use an electronic identity verification (eIDV) service to verify a cardholder’s full name and shipping address.

- Monitor your business transactions to recognize inconsistencies such as unusual shipping addresses, billing flaws, and irregular payment patterns.

- You can also use sophisticated software to track the IP addresses of your consumers. The system will immediately inform you if it detects a suspicious IP address.

- Sending a confirmation email can also help avoid fraudulent purchases.

- Include Card Verification Value (CVV) in the transaction field to verify the identity of your consumers as hackers find it virtually impossible to steal this four digit code printed on the back of a credit card.

- Putting transaction controls can also help curb online frauds. Only consumers with a proven track record should be allowed to make large and frequent purchases. Make sure to set a lower review limit for new customers.

- Keep a record of fraudulent and suspicious account activities to avoid fraud by the same scammers.

Apps to Prevent Identity Theft

With the introduction of smartphones, our lives have become a lot easier. Though convenient, smartphones have also become a target for hackers to obtain your sensitive personal information for illicit purposes. That’s where identity theft apps come in. These apps can protect you against potential identity frauds.

1. Credit Karma

OS: Android and iOS

Cost: Free

One of the easiest ways to avoid identity theft is to monitor your credit score regularly. Credit Karma is a simple app that sends you an updated credit report on a daily basis. It has partnered with TransUnion and VantageScore to provide free credit score. The app also provides tools and information to keep your personal details safe.

2. NordVPN

OS: Android and iOS

Cost: Free 30 days trial, $11.99 per month, $69.00 per year

NordVPN is one of the most reliable VPN services out there. It masks your Internet traffic in public areas, protecting your phone from potential hackers. It offers military-grade security at remarkably cheap rates. It also boasts a double VPN feature that encrypts your data twice, making it more secure than ever.

3. Password

OS: Android and iOS

Cost: Free 30-day trial, In-app purchases may vary

1Password remembers all your passwords and keeps them safe and secure. You can also share the passwords securely with your team and family members. You can also receive alerts when a website you are using gets compromised. You can store information including logins, credit cards, addresses, notes, bank accounts, driver licenses, and passports. The data is encrypted on your device before it is transferred to another device or cloud.

4. Signal

OS: Android and iOS

Cost: Free

Signal is a secure messaging app that provides end-to-end encryption to secure your text and voice communications. Your data is never stored on the server to guarantee complete protection. Thus, it ensures that none of your sensitive information gets into the hands of hackers, not even accidentally.

5. Cerberus anti theft

OS: Android

Cost: Free

As the name suggests, Cerberus provides a triple-layered anti-theft solution for your Android phone. However, it also protects your data in case your phone is stolen or lost. Some of the stellar features include locating your device on the map, taking pictures of the thief, identifying fake Wi-Fi hotspots, and erasing the internal memory and SD card remotely to protect your personal data.

These apps can shield your sensitive data from hackers. However, this is not an exhaustive list. We have listed only the best apps in different categories such as credit monitoring, network security, password protection, data encryption, and anti-theft. You can download any of these apps or the ones similar to these according to your requirements.

How to Report Identity Theft

Unfortunately, most people fall victim to identity theft at some point as fraudsters continue to find innovative ways to steal personal information. In the event you become one of the millions of ID theft victims in the US, take the following steps to arrest the potential damage in its track.

1. Notify Affected Organizations and Suspend Your Accounts

- The first thing you need to do is to put the fire out before it spreads. So, contact the affected organizations as soon as you notice any discrepancies in your finances.

- Most banks, insurance companies, and other organizations have antifraud departments. You can contact them to freeze or suspend your accounts and credit cards right away.

- If your SSN is stolen, you need to contact the Office of the Inspector General immediately.

- You can contact (Social Security Administration) SSA directly at 1-800-772-1213 to request a replacement Social Security Card.

- Likewise, you may have to change the driving license number or get a new passport if it falls into the wrong hands.

- Make sure to change all your account passwords, including your email passwords, to secure your online transactions.

2. Put a Fraud Alert or Credit Freeze on Your Credit Report

- The next step is to contact the credit bureaus such as Experian, Equifax, and, TransUnion to put a fraud alert on your credit files. If you call one of the credit bureaus, it will inform the rest immediately.

- The fraud alert will last for 90 days. However, once you have registered a complaint with the FTC or the local police, you can extend the alert for as long as seven years.

- Sometimes, however, you may have to put a credit freeze on your reports as it prevents credit companies from releasing your credit report to new financial organizations.

3. Report the Theft to Federal Trade Commission (FTC) and Local Police

- Though the FTC doesn’t pursue individual fraud cases, it is entrusted to oversee all identity theft cases in the United States. Nonetheless, you also need to file a report with the local police as it may help to resolve monetary disputes.

- Your completed theft report should include the notarized ID theft affidavit and a copy of the police report filed with the local police department.

- Go to the IdentityTheft.gov to register your ID theft report with the FTC. At the end of the process, the portal will provide you with a customized recovery plan as well.

- It is better to keep a copy of all the forms, including the affidavit and the police report, in your possession.

- The ID theft report helps you to rectify credit report errors, stop the process of debt collection, and dispute the fraudulent debt. So, fill it out carefully. Avoid exaggerating the extent of crime at all costs.

4. Repair the Damage and Close Fake Accounts

- Merely reporting the ID theft isn’t enough to reinstate your credit history. You will need to send a copy of the theft report to all financial organizations.

- You may have to persistently follow up on everything depending on the nature of the theft. The recovery plan will guide you through the follow-up process. So, read the smallest detail given in it and act accordingly.

- Request the organizations to close all fake accounts in your name. However, you should keep going through your credit reports and account statements to make sure nothing is out of place until the process is completed.

How Long Does It Take to Recover from Identity Thefts

Recovering from identity theft may take a few months or even years as the speed of recovery depends on several variables given below.

1. Time Needed to Notice the Fraud

Identifying the fraud in its early stages not only prevents it from causing further damage, but also results in a speedy recovery. That’s why hiring an identity theft alert service can be a big help for the victim.

2. Your Credit History before the Theft

Your credit health before the theft also plays a fundamental role in the recovery process. The better your credit health, the sooner you can restore your credit reports.

3. How Much Time Can You Put In

The recovery process involves making dozens of phone calls, extensive investigative work, and continuous follow-up. As a result, you have to put in a lot of time and effort to give it a boost. Unfortunately, for most people, time is a luxury they can’t afford. That’s one of the reasons why full recovery may take months.

4. Nature of the Theft

Mostly fraudsters use the stolen identities themselves. Sometimes, however, they sell your identity to someone else. It not only increases the damage, but also makes it difficult to track the real perpetrator. In other words, it affects your recovery process gravely.

5. Is the Perpetrator under Arrest?

The sooner the authorities manage to arrest the fraudster, the faster you can recover your monetary damages. Unfortunately, most identity thieves, particularly cybercriminals, are rarely put behind bars as they don’t live or operate inside the United States. So, the process simply stretches on.

Identity Theft Protection Services

Contrary to popular belief, identity theft protection services cannot protect your identity from getting stolen. However, they do offer certain advantages that certainly help you detect theft attempts as early as possible. Here’s how they work.

1. Credit Monitoring

Most identity theft protection services monitor your credit report so that when ID thieves use your stolen identity to commit fraud, the service provider detects the suspicious activities in your credit report. They will alert you so you can handle the situation.

2. Finance Monitoring

Identity theft protection services also monitor your finances because it is not possible to detect such fraud by monitoring credit report alone. So, companies often keep an eye on your credit card transactions, bank accounts, and other finances.

3. Personal Information Monitoring

Alternatively, theft protection services also monitor public records, medical databases, and other records to discover unauthorized activities related to your SSN and driving license.

4. Software Protection

Hacking is one of the most common ways to steal personal information. So, most companies also provide antivirus and firewall protection software to safeguard your online transactions. Encrypted logins and anti-keylogging provide additional layers of security.

However, the earlier you can detect the ID theft, the quicker you can arrest the damage it causes. So, spending a few hundred dollars on identity theft protection service may save you thousands in future. Here are a few top-notch services to consider.

(4.1 )IdentityForce

Cost: $12.95 or $19.95 per month

Website: https://www.identityforce.com/

ID Theft Insurance: $1,000,000

It has been in business for more than three decades. It monitors all your financial information including your SSN and tri-bureau (Equifax, Experian, and TransUnion) credit report updates. Comprehensive public records monitoring including criminal, court and sex offender records is a plus. IdentityForce offers a 14-day free trial. You can enjoy 24/7 theft restoration services fully managed by experts.

(4.2 )LifeLock

Cost: $10, $20 or $30 per month

Website: https://www.lifelock.com/

ID Theft Insurance: Up to $1,000,000 (varies according to monthly plan)

LifeLock monitors court records, your SSN, and financial accounts. It offers monthly updates on your credit score. However, tri-bureau (Equifax, Experian, and TransUnion) monitoring is available exclusively for the highest priced plan. The company provides a limited power of attorney and lost wallet assistance apart from assistance with financial, medical, criminal, and tax identity recovery. It will also work with customers having preexisting identity theft conditions for a fee of $300.

(4.3 )IdentityGuard

Cost: $24.99 per month

Website: https://www.identityguard.com/

ID Theft Insurance: $1,000,000

It offers monthly tri-bureau credit report monitoring, credit-score analyzer, anti-keylogging software, encryption software, public record monitoring, and antimalware suite. It also watches known black market websites for misuse of your information. Identity Guard sends prompt notifications by email, phone, or text if any suspicious activity is detected. If your wallet is lost or stolen, it will not only cancel your cards, but also furnish up to $2,000 in emergency cash.

(4.4 )IDWatchDog

Cost: $14.95 or $19.95 per month

Website: https://www.idwatchdog.com/

ID Theft Insurance: $1,000,000

The service monitors your address, SSN, and tri-bureau credit reports. It also scans non-traditional credit records such as pawn store loans and payday lenders to provide an additional layer of security. If it detects any suspicious activity, an alert is sent via email or text message. However, the biggest advantage of ID Watchdog is that it can help restore your identity even if you are not using its ID monitoring services.

(4.5 )Credit Sesame

Cost: Free, $9.95, $15.95 or $19.95 per month

Website: https://www.creditsesame.com/

ID Theft Insurance: $1,000,000

Unlike most identity theft protection services, Credit Sesame offers a free basic account. However, the free account offers credit monitoring only for TransUnion. The premium service offers tri-bureau credit score monitoring with monthly updates. You don’t need to hand over any credit card information to open a free account, but will have to enter your SSN.

Credit Card Fraud versus Identity Theft

People often use the terms credit card fraud and identity theft interchangeably. Though both can damage your credit history, they are a significantly different types of crime. However, both crimes are common.

1. How They Happen

- Credit card fraud often occurs when your card is stolen. The perpetrator often uses the stolen card to make unauthorized purchases in your name.

- Identity theft occurs when someone steals your personal information including SSN or driving licenses to assume your identity. ID thieves often use sophisticated methods such as hacking, phishing or a data breach to commit such a crime.

2. Fraud or Theft Alert

- Spotting credit card fraud is easier than discovering identity theft. As the perpetrator uses the same credit card to make fraudulent purchases, your creditor can pick up the unusual activity and alert you immediately. It is also easier to spot the discrepancies in your credit card statement.

- ID theft victims may remain unaware of the theft for weeks, months or even years as the tactics used to commit such a fraud are often too sophisticated to show up on your creditor’s radar.

3. Damages

- Usually, credit card fraud involves the misuse of only one or two cards. Thus, financial losses are considerably limited compared to identity theft.

- Identity theft, however, can lead to significant financial losses as criminals can use your identity to open a new line of credit, receive tax refunds, obtain medical benefits, and even commit a crime. In short, the financial impact can be much larger and it can last much longer, sometimes for decades.

4. Recovery

- Recovering from a credit card fraud is relatively quick and easy due to the limited impact. According to federal laws, you can be held liable for a maximum of only $50 in the event of a fraud. Reporting the fraud within 60 days from learning of it may waive the $50 fine as well.

- Rules for debit card loss may differ slightly. After the discovery of fraud, you are liable for $50 for first two days. It may increase to $500 between the two-day and 60-day period. If the card was skimmed or cloned, these rules become more lenient.

- Recovering from identity theft, on the other hand, is a strenuous and time-consuming process. It may take years to erase the negative impact of ID theft on your medical benefits, tax reports, and lines of credit. You may also have to deal with dozens of financial organizations, government and law enforcement agencies to recover the damages.

Credit Monitoring versus Identity Theft Protection

Just like credit card fraud and identity theft, most people also use the terms credit monitoring and ID theft protection interchangeably. While the primary purpose of both services is to alert you when a potential identity theft occurs, they offer different levels of security.

Credit monitoring is different from identity theft protection in the following ways.

1. Cost

- By law, you have access to one free credit report per year from each of the three major credit reporting agencies. You may have to pay for monthly credit reports and credit scores.

- One way to obtain the free credit report is to order it from one of your three major reports every four months. So, you get a free copy every four months.

- You may have to pay monthly or yearly charges to apply for an identity theft protection service.

2. Services Offered

- Credit monitoring bureaus offer only credit reports and credit score. They don’t monitor your personal information such as SSN or driving license.

- However, you can place fraud alerts or credit freeze on your credit reports in the event of an identity theft.

- Apart from monthly credit report updates and credit score from credit bureaus, ID theft protection services also provide additional security measures such as monitoring change of USPS mailing address requests, court or arrest records, payday loan applications, check-cashing requests, social media and email accounts, and websites where criminals sell or trade stolen information.

- Most ID theft protection companies also offer fraud resolution assistance, lost wallet feature, and identity theft protection insurance.

However, as explained earlier, neither credit monitoring nor ID theft protection services can prevent identity fraud from happening. But, they do provide instant alerts in case of financial inconsistencies.

Identity Theft Insurance

Most identity theft protection services and insurance companies offer identity theft insurance. However, this is a grossly misunderstood product. Don’t let the term “insurance” fool you into believing that it will cover all the damages caused by ID fraud. You need to understand how ID theft insurance works before signing up for such a service.

It does not cover direct monetary losses. Instead, it covers the following expenses.

- Charges for obtaining credit reports and other documents related to the theft.

- Phone bills related to the theft.

- Lost wages.

- Attorney and tax advisor fees.

- Supplementary expenses such as child care, parking, and fuel charges when the victim needs to visit offices in person.

- Loan re-application fees, notary fees and costs for certified mail.

- Any other expenses or fees not covered by the bank or credit card issuer.

- Sometimes, the insurance company may also connect you with a financial counselor to guide you through the recovery process. This service is often offered free of charge.

Identity theft insurance is rarely available as a stand-alone policy. Usually, it is tacked on to existing home, renters’, auto, and travelers’ insurance policy. It may cost you a flat annual fee of just a few dollars (usually $25 to $60) which may vary from state to state. However, just like any other insurance policy, ID theft insurance also comes with a lot of ifs and buts.

- Most insurance policies require a significant deductible, such as $500 or more, for the benefits to kick in. So, if the cost of damage repair is less than the deductible, you won’t get paid a cent.

- Payouts often have a cap limit and may require a preapproval. However, most banks and credit card companies already cover various losses due to fraud.

So, make sure to understand all the terms and conditions before buying your policy.

To Wrap It Up

Identity theft is affecting millions of Americans every year. Unfortunately, the perpetrators are using increasingly sophisticated methods, making it difficult to prevent identity fraud from hurting people. However, you can take certain precautions to avoid becoming a victim. This comprehensive guide will clarify your doubts regarding identity theft including its implications, security measures, and recovery process. If you have been a victim of identity theft, share your experience in the comments section below.

Our new product: millimeter wave radar sensor